Your Guide to a Speedy Mortgage Decision in Principle (DIP)

1. What is a Decision in Principle (DIP) and Why is it Important?

A Decision in Principle (DIP), also known as a Mortgage in Principle (MIP) or Agreement in Principle (AIP), is a document from a lender that gives you an estimate of how much they might be willing to lend you.

The Importance of a DIP:

Boosts Your Credibility: Having a DIP shows estate agents and sellers that you are a serious buyer whose finances have already been partially vetted. This can be a huge advantage in a competitive market.

Sets Your Budget: It clearly defines your borrowing limit, preventing you from wasting time viewing properties you cannot afford.

Speeds Up the Full Application: Providing this information upfront means the lender has already completed initial credit checks, which significantly shortens the time needed for the final, formal mortgage offer.

It's the First Step: Most estate agents won't allow you to make a formal offer on a property without one.

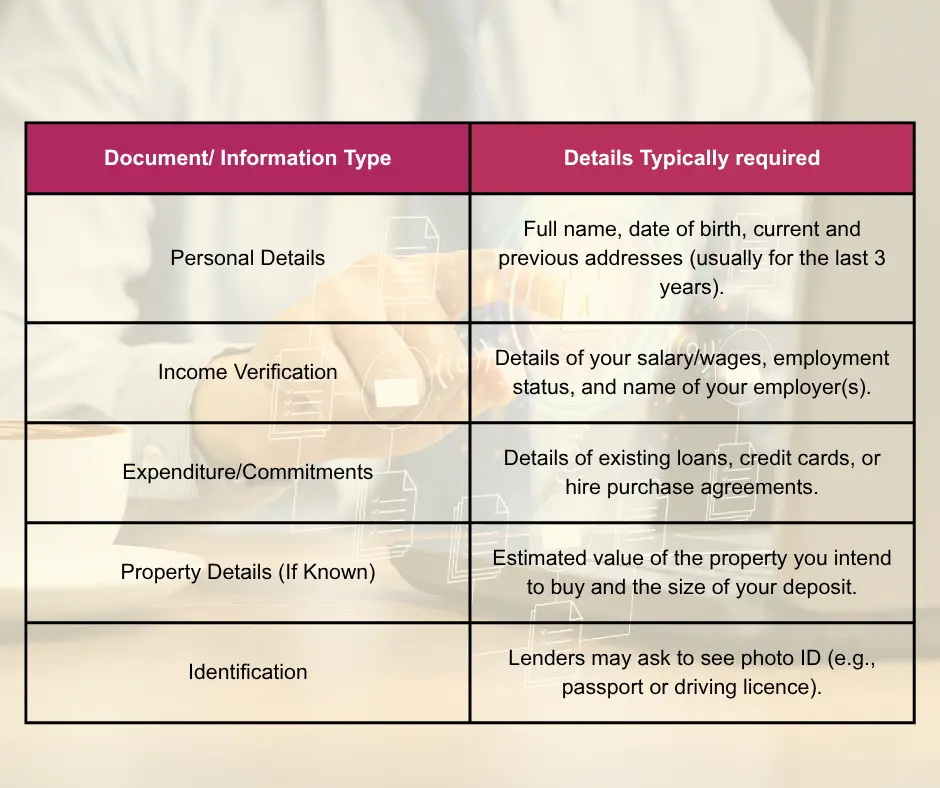

2. Required Documentation for the DIP Pre-Approval Process

The DIP process is quicker than a full mortgage application, but you'll still need to provide accurate information to allow the lender to complete a 'soft' credit check and assess your basic affordability.

Documents Needed for a quick DIP

Note: Lenders will often request bank statements and payslips later in the process, but having them ready can certainly help at the pre-approval stage.

3. Strategic Steps to Expedite Your DIP Issuance

The key to a fast DIP is preparation and accuracy. By taking these simple, strategic steps, you can help your application move swiftly.

Check Your Credit Report: Ensure there are no errors on your credit file before applying. Correcting mistakes before the lender sees them is vital.

Gather All Documents Upfront: Have all the documentation and information listed above organised and ready to go. The biggest delay often comes from the back-and-forth of chasing missing information.

Be Accurate and Honest: Provide completely accurate figures for your income and outgoings from the start. Any discrepancies found later will cause significant delays or even lead to a rejected application.

Limit New Credit Applications: Avoid applying for new credit cards, loans, or changing your bank account in the months leading up to and during your mortgage application. This keeps your financial profile stable.

Use a Whole-of-Market Adviser: A mortgage adviser who works across the whole market can quickly compare many lenders' criteria and application speed, choosing the one most likely to issue your DIP quickly and without fuss.

Ready to Take the Next Step?

Securing your DIP doesn't have to be a complicated process. The best way to ensure you get the right product quickly is to work with an expert who knows the market inside and out.

We work nationwide, offer whole market access to find you the best deal, and will personally handle the application process to expedite your Decision in Principle.

We use cookies to enhance your browsing experience, serve personalized content, and analyze our traffic. By clicking "Accept All", you consent to our use of cookies.

.webp)